PayID vs Crypto at the Casino: Two Different Bets Entirely

Loading...

PayID and crypto solve different problems

Every few weeks someone asks me to settle the PayID-versus-crypto argument as if there is a winner waiting to be crowned, and I have stopped pretending there is. After nine years watching both move real money in and out of casinos, I can tell you the framing is wrong. These are not two answers to one question. They are answers to two different questions, and choosing between them is really choosing which question matters more to you.

Table of Contents

PayID is a regulated, real-time Australian payment rail. You fund it from money you actually hold, it settles in your own currency, it carries your verified identity, and it sits inside the supervised banking system. Crypto is the near opposite on almost every axis: a pseudonymous, globally portable, self-custodied asset whose value moves on its own and whose whole appeal is operating outside the banking system that PayID lives inside. One is built for control and traceability. The other is built for autonomy and detachment from institutions. They are not competing on the same field.

This is why “which is better” produces such useless arguments. Better at what? PayID is better if what you value is speed in your own currency, traceable payments, and the comfort of a regulated rail. Crypto is better if what you value is pseudonymity and operating independently of banks, and you are willing to take on volatility and custody risk to get it. Neither answer is universal, because the people asking want fundamentally different things, and the honest job here is to map the trade-offs rather than declare a champion.

And there is an Australian wrinkle that overhangs the entire comparison, one most crypto-versus-PayID pieces ignore: the regulatory backdrop treats these two methods very differently, which changes the calculation in ways that have nothing to do with speed or fees. I will get to that, because it is the axis that quietly matters most for an Aussie player. But first let me take the comparison the way it deserves to be taken, axis by axis, starting with the one everyone cares about: speed.

Settlement speed: real-time rails vs blockchain

Speed is where the marketing on both sides gets loudest and least precise, so let me ground it. The honest comparison is not “which is instant” but “what does the settlement step actually depend on,” because the two methods become fast or slow for completely different reasons.

PayID’s speed comes from purpose-built real-time infrastructure operating at national scale. In 2024 the underlying platform processed around 1.6 billion transactions worth roughly 1.99 trillion Australian dollars, the vast majority clearing in real time, often in seconds. This is not a best-case figure; it is the everyday performance of a rail that already handles more than 35 percent of all account-to-account transactions in the country. The settlement step for PayID is genuinely, reliably instant, because the system was engineered to be exactly that and is proven at enormous volume.

Crypto’s speed is more variable and depends on which asset and which network you use. A transaction on a fast, low-cost chain can confirm in seconds; a transaction on a congested network during a busy period can take far longer and cost more while you wait. Settlement is not a fixed property of “crypto” the way real-time is a fixed property of the NPP rail; it is a property of the specific coin and the network conditions at that moment. On a good day crypto can match PayID’s settlement speed. On a bad day it cannot, and you do not always get to choose which day it is.

But here is the point both camps miss, the one I keep coming back to: at a casino, the settlement step is rarely what was slowing you down. Whether you use PayID or crypto, your withdrawal still has to clear the operator’s manual approval window before any rail or chain gets involved. A casino that takes three days to approve a payout makes the PayID-versus-crypto settlement difference almost irrelevant, because the bottleneck lives inside the casino, not inside the payment technology. The fastest rail in the world still waits in the operator’s queue, which means neither method rescues you from a slow casino, and that is the variable worth optimising before you ever fuss over coins versus dollars.

Cost and fees, head to head

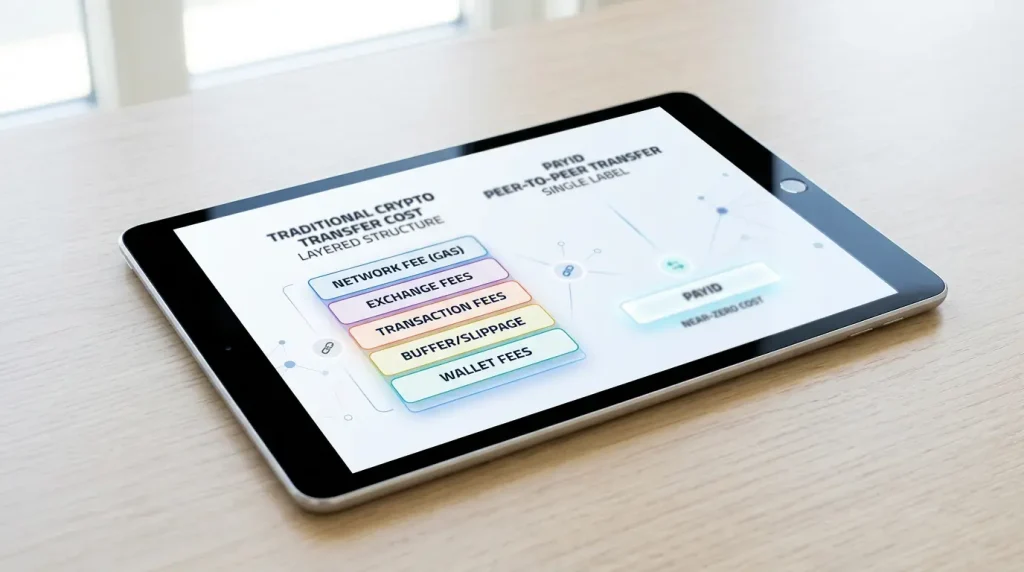

Cost is the axis where the comparison is genuinely lopsided in PayID’s favour, and the reason is structural rather than promotional. The real-time rail PayID runs on became extraordinarily cheap to operate as it scaled, with the wholesale cost of a single transaction falling from 39 cents in 2019 to roughly 4 cents by the 2025 financial year. That collapse in unit cost is why account-to-account transfers became default plumbing rather than a premium service, and for you it usually means a PayID deposit or withdrawal carries no transfer fee at all from the payment side.

Crypto’s cost structure is more layered, and the headline “no bank fees” hides the layers. A crypto transaction carries a network fee, the cost of having the transaction processed on the chain, which varies with congestion and can spike unpredictably. On top of that, getting into and out of crypto usually means converting Australian dollars to a coin and back again, and each conversion carries a spread, the gap between the buy and sell price that the exchange keeps. If you deposit in crypto and withdraw in crypto and then cash out to dollars, you have potentially paid a conversion spread twice plus network fees both ways. The “feeless” impression comes from looking only at the casino’s cashier and ignoring the costs that sit outside it.

Volatility adds a cost that does not even look like a fee, which is what makes it sneaky. If the coin you are holding drops in value between when you deposit and when you withdraw, you have lost money on the payment method itself, separate from any gambling outcome. PayID has no equivalent, because your balance is denominated in Australian dollars the whole way through and a dollar is a dollar tomorrow. So the genuine cost comparison is not “PayID’s small fees versus crypto’s small fees.” It is PayID’s near-zero, predictable cost in stable dollars versus crypto’s variable network fees, double conversion spreads, and the lurking possibility that the asset itself moves against you while you are simply trying to move money.

Privacy and identity: KYC vs pseudonymity

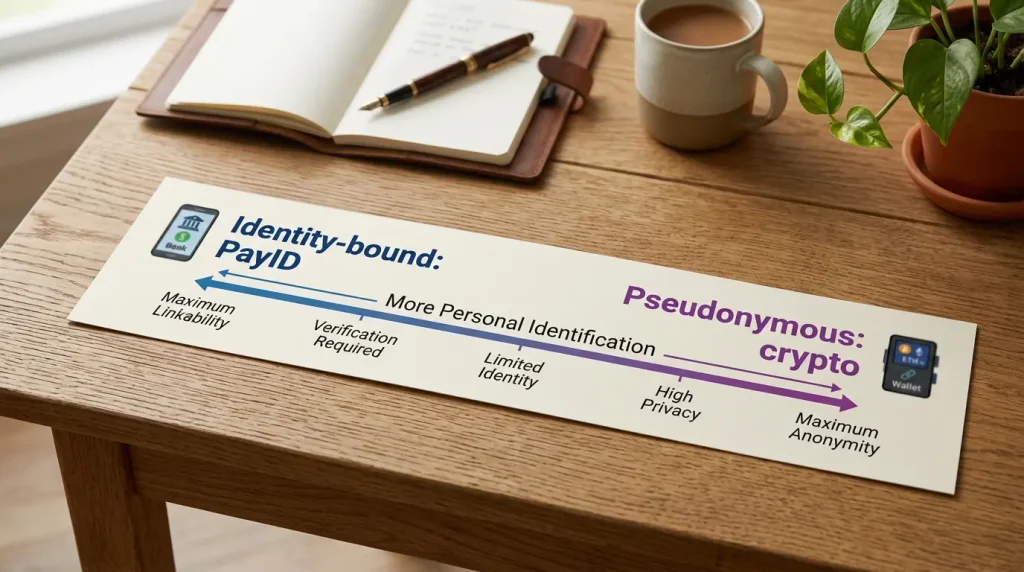

Privacy is the axis where crypto’s reputation does most of its work, and also where the most misunderstanding lives, so let me be careful here. The two methods sit at genuinely different points on the privacy spectrum, but neither is quite what its fans or detractors claim.

PayID is explicitly identity-bound. It is funded from your bank account, it runs through the supervised banking system, and using it at a casino means your verified identity sits behind every transaction. There is no pretending otherwise, and the casino’s own know-your-customer process, the identity checks an operator runs before paying out, layers further verification on top. If your priority is keeping your gambling activity off your banking record and away from any institution, PayID is the wrong tool, because traceability is not a bug in it; it is the entire design.

Crypto offers pseudonymity, which is a precise word and not the same as anonymity. A blockchain transaction is not tied to your legal name by default, so it carries a layer of privacy a bank transfer never could. But the chain itself is a permanent public ledger, every transaction visible forever, and the moment you convert crypto to dollars through a regulated exchange, your identity attaches at that boundary. So crypto gives you pseudonymity in the middle of the journey while the endpoints, where you bought in and where you cash out, are typically identified. It is more private than PayID, meaningfully so, but the “anonymous money” framing oversells it.

The deeper point is that PayID’s identity-binding is not purely a cost; it is also where its scam protection comes from, and that is the trade you are actually making. The payments industry has built protection directly into the rail, with one senior figure putting it this way: “stopping scams can’t be left to chance or handled after the fact. It needs to be built into how we pay, from the ground up.” The name-check that shows you a recipient’s real name before you send, and the recourse that comes from operating inside the regulated system, exist precisely because PayID knows who everyone is. Crypto’s pseudonymity buys you privacy by giving up exactly that protective scaffolding. You are not choosing between privacy and no privacy; you are choosing between privacy with no safety net and identity with one. Which is right depends entirely on what you are actually worried about.

Volatility, custody and reversibility risk

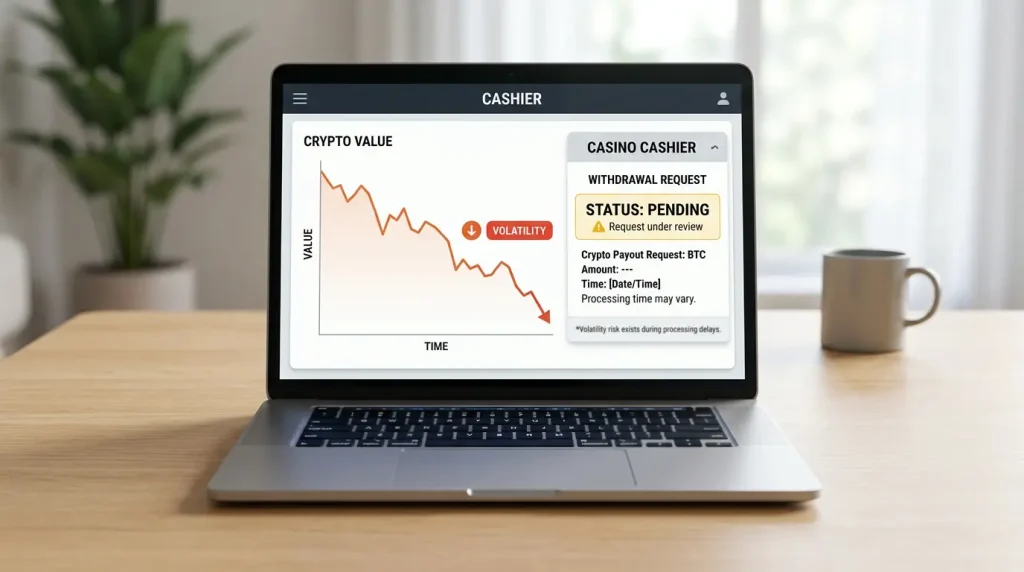

This is the axis where I see players get genuinely hurt, and almost always because they thought of crypto purely as a payment method and forgot it is also an asset they now have to hold. The risks here are not abstract; they are the ones that turn a winning session into a net loss for reasons that have nothing to do with the games.

Start with volatility, because it is the one that bites quietly. If you deposit in a cryptocurrency, your casino balance, or your winnings waiting to be withdrawn, can fall in value while you are doing nothing but waiting for an approval window to clear. You can win at the tables and still come out behind because the coin dropped during the payout delay. PayID carries no such risk: an Australian dollar in your balance is an Australian dollar when it lands, full stop. The casino has become a place where you are exposed to currency risk on top of gambling risk, and most players never priced that in.

Custody is the second risk, and it is the one that ends badly most abruptly. Holding crypto means someone holds the keys, either you or a platform, and if those keys are lost, stolen, or trapped in a platform that fails, the funds are typically gone with no one to appeal to. The same irreversibility that crypto advocates praise becomes merciless when something goes wrong: a mistaken transfer or a theft cannot be clawed back. PayID transfers are also not casually reversible, but they run inside a banking system with dispute processes, fraud teams, and the name-check defences built to stop the misdirection in the first place. The custody question for PayID is simply your bank, which is a regulated, insured, recoverable counterparty in a way a self-custodied wallet or an offshore crypto platform is not.

There is also a regulatory signal sitting underneath the crypto risk that an Australian player should weigh, because the authorities have already made their view visible. From 11 June 2024, licensed betting operators in Australia were prohibited from accepting cryptocurrency, alongside credit cards, a prohibition the regulator assessed as very highly complied with. That ban does not govern offshore casinos, but it tells you plainly that Australian authorities classify crypto as a higher-risk way to fund gambling, harm and traceability being the concerns. Set against that, the sheer ordinariness of PayID, the everyday rail tens of millions of Australians already use for entirely mundane transfers, looks less like a feature and more like the absence of all these compounding risks. The full reasoning behind why the regulator pushed credit and crypto out of licensed gambling is worth understanding on its own terms, and I lay it out in my piece on the gambling credit card and crypto ban in Australia.

The legality angle that changes everything

Here is the axis that quietly outranks speed, cost, and privacy combined for an Australian player, and the one the crypto-versus-PayID debate almost never reaches. The payment method you choose does not change the legal status of the casino, but the regulatory signals attached to each method tell you a great deal about how the system views your choices.

Neither PayID nor crypto makes an offshore online casino legal, because online casinos are prohibited to supply to Australians regardless of how the money moves. On that, the two methods are equal: both carry your money to an unsupervised offshore operator with no domestic recourse behind it. But the regulatory posture toward the methods themselves diverges sharply. PayID is mainstream, sanctioned, and woven into the supervised financial system. Crypto has been formally pushed out of licensed gambling and flagged as higher-risk. That divergence does not criminalise your payment choice, but it does mean crypto sits further from the regulated mainstream, with thinner institutional protection around it, which compounds every other risk we have discussed when the counterparty is already offshore and unsupervised.

So the legality angle does not produce a simple verdict, but it does reframe the comparison. With PayID you are using a fully legitimate rail to reach an illegitimate operator; with crypto you are using a rail the authorities actively disfavour to reach the same illegitimate operator. The casino’s lack of protection is constant either way, but PayID at least keeps the payment leg of the journey inside the system that can help you, while crypto removes even that. For an Aussie player, that is the axis I would weight most heavily, because it is the one that determines whether anything at all stands behind your money before it leaves the country.

Which method fits which Aussie player

Let me bring the axes together into the only thing that matters: which method actually suits you, given what you are trying to do. There is no universal answer, but there is a clear answer once you know your own priorities, so let me match the profiles I see most often.

If you value speed in your own currency, predictable near-zero cost, traceable payments, and the comfort of a rail that sits inside the regulated banking system, PayID is the obvious fit, and it is the right fit for most ordinary players. You fund it from money you have, your balance stays in dollars from deposit to withdrawal, the name-check guards the payment, and if a deposit goes astray there is a banking system with processes behind it. The trade you accept is that your gambling activity is identity-bound and visible on your banking record, which for most people is a price worth paying for everything else PayID provides.

If your overriding priority is pseudonymity and operating independently of banks, and you genuinely understand and accept the volatility, custody, conversion-cost, and regulatory-disfavour risks that come with it, crypto offers something PayID cannot. That is a narrower profile than the marketing suggests, because it requires you to treat the payment method as an asset you are actively holding and to be comfortable with the irreversibility and the missing safety net. For a player who wants privacy above all and has the discipline to manage the asset risk, crypto is a coherent choice. For everyone else, the privacy it buys is rarely worth the bundle of risks it brings.

The deciding question I would put to you is simple: are you trying to move money, or are you trying to hold an asset while moving money? If you just want your dollars to get in and out of a casino quickly, cheaply, and safely, that is PayID’s entire job description. If you are willing to take on the job of managing a volatile, self-custodied asset in exchange for pseudonymity, that is what crypto asks of you. Most players, when they answer that honestly, discover they wanted PayID all along.

The verdict for AUD players

If you came here for a winner, here is the closest I will get to one, with the reasoning attached so you can disagree if your priorities differ from most. For the typical Australian player who wants to move dollars in and out of a casino, PayID is the stronger fit on nearly every axis that actually affects the experience: settlement is reliably real-time, cost is near-zero and predictable, your balance never moves against you, and the payment leg stays inside a regulated system with name-check and dispute processes behind it. Crypto can match the speed on a good day and offers real pseudonymity, but it asks you to absorb volatility, custody risk, double conversion costs, and a regulatory cold shoulder to get there.

The honest caveat, the one I will not drop because it outweighs the payment choice entirely, is that neither method protects you from the casino. Both rails carry your money to an offshore operator no Australian authority supervises, and that risk dwarfs the differences between PayID and crypto on speed or fees. Choose the payment method that fits your priorities by all means, but spend your real diligence on the operator, because the safest possible payment to the wrong casino is still money you may never see again. PayID wins the payment comparison for most AUD players. Winning the casino comparison is a separate task, and a more important one.

Frequently Asked Questions

Is crypto more anonymous than PayID at casinos?

Crypto is more private than PayID, but the right word is pseudonymous rather than anonymous. A blockchain transaction is not tied to your legal name by default, which PayID can never offer since it runs through your identified bank account. However, the chain is a permanent public ledger, and the moment you convert crypto to dollars through a regulated exchange your identity attaches at that boundary. So crypto gives you privacy in the middle of the journey while the points where you buy in and cash out are typically identified, which means the fully anonymous money framing oversells what it actually provides.

Which is cheaper to use, PayID or Bitcoin?

PayID is almost always cheaper once you count every cost, not just the casino cashier. The real-time rail PayID runs on became extraordinarily cheap as it scaled, and a PayID transfer usually carries no fee at all from the payment side. Crypto looks feeless in the cashier but carries a network fee that varies with congestion, plus a conversion spread each time you move between dollars and a coin, which can mean paying that spread twice on a round trip. Add the chance the coin loses value while you wait, and crypto's true cost is both higher and far less predictable than PayID's near-zero, stable cost.

Can crypto value drop while my withdrawal is processing?

Yes, and this is one of the most overlooked risks of using crypto at a casino. If your balance or your pending winnings are held in a cryptocurrency, their dollar value can fall while you wait for the operator's approval window to clear, which means you can win at the games and still come out behind because the coin dropped during the delay. PayID carries no equivalent risk, because your balance stays denominated in Australian dollars from deposit to withdrawal, so a dollar you win is a dollar that lands. Treating crypto purely as a payment method while ignoring that it is also a volatile asset is how players get caught out.

Is one of them safer if the casino disappears?

Neither protects you meaningfully if an offshore casino vanishes, because both rails carry your money to an operator no Australian authority supervises and from which there is no domestic recourse. That said, PayID keeps the payment leg of the journey inside the regulated banking system, with dispute processes and fraud teams that at least exist, whereas crypto removes even that thin layer and adds custody risk on top. But the honest answer is that the real protection against a disappearing casino comes from vetting the operator before you deposit, not from the payment method, since once your money reaches a non-paying offshore operator no rail recovers it for you.

Recommend

PayID Casino Australia: How the Payments, Safety and Legality Really Work

How I Judge the Best PayID Casinos for Real Australian Players

What separates the best PayID casinos The first time a reader emailed…

Are PayID Casinos Legal in Australia? Reading the Law Straight

The legal status of PayID casinos, stated plainly I am not a…

How a PayID Deposit Works at an Online Casino

Making your first PayID deposit The first time I ever funded a…

The Minimum Deposit at a PayID Casino, Explained

The lowest you can deposit with PayID The smallest PayID deposit I…