PayID Casino Withdrawals: What Getting Paid Actually Looks Like

Loading...

What a PayID withdrawal really involves

A reader once forwarded me a casino’s live chat transcript where the agent swore his withdrawal was “instant” while the same withdrawal sat untouched for two days. He was not being lied to, exactly. He was being told the truth about the rail and nothing about the process, and that gap is where almost every PayID payout frustration lives.

Table of Contents

So let me set the record straight before we go further. When a casino advertises a PayID withdrawal as instant, it is describing the New Payments Platform underneath, which genuinely settles in real time, often in seconds. What it is not describing is the manual approval window on the casino’s own side, where a human or a risk system decides whether to release your funds in the first place. The rail is fast. The gatekeeper in front of the rail is what makes you wait.

There is a second surprise hiding in the word “withdrawal,” and it catches people who deposited via PayID without a hitch. Many operators accept PayID on the way in but do not pay out through it at all. Instead they return your money by ordinary bank transfer, which can take days and reintroduces the exact friction PayID was supposed to remove. The deposit experience tells you nothing about the withdrawal experience, and assuming otherwise is the most common mistake I see.

This article is about the real shape of getting paid, not the advertised one. I will walk you through why so many casinos take PayID one direction only, what the genuine timeline looks like from request to landed funds, where the approval window sits and why it exists, how limits and threshold reviews stretch things out, and how PayID payout speed honestly compares to the alternatives. The goal is simple. By the end you should be able to predict, before you ever click withdraw, roughly how long your money will actually take and what could slow it down.

Why many casinos take PayID for deposits only

The single question I am asked most often is some version of “why did my PayID deposit work instantly but my withdrawal come back as a bank transfer?” The answer is not technical. It is commercial, and once you see the incentive structure it never confuses you again.

Accepting PayID for deposits is almost pure upside for an operator. The money arrives in real time, the deposit clears before the player can second-guess it, and there is no card chargeback risk because account-to-account transfers, where funds move directly between bank accounts rather than through a card network, cannot be reversed the way a disputed card payment can. Fast in, irreversible, cheap to process. From the casino’s side, inbound PayID is close to ideal.

Outbound PayID is a different calculation entirely. Paying you back through PayID means the operator has to hold a funded account on the same rail, manage the addressing service that maps your PayID to your bank account, and reconcile real-time outflows against its own risk and compliance checks. None of that is hard, but it is work, and for an offshore operator with no obligation to make withdrawals convenient, the path of least resistance is to push payouts onto a generic bank transfer it was already set up to send. The asymmetry is the whole explanation: deposits are an opportunity, withdrawals are a cost.

This is why I treat two-way PayID support as a genuine quality signal rather than a feature checkbox. An operator that has gone to the trouble of paying out through PayID has chosen to absorb friction on your behalf, which tells you something about how it treats the post-deposit relationship. The split between deposit-only and full two-way support is worth understanding in its own right, and I lay out the distinction in detail in my guide to whether casinos let you withdraw via PayID or only deposit. If you only check one thing before depositing, check this.

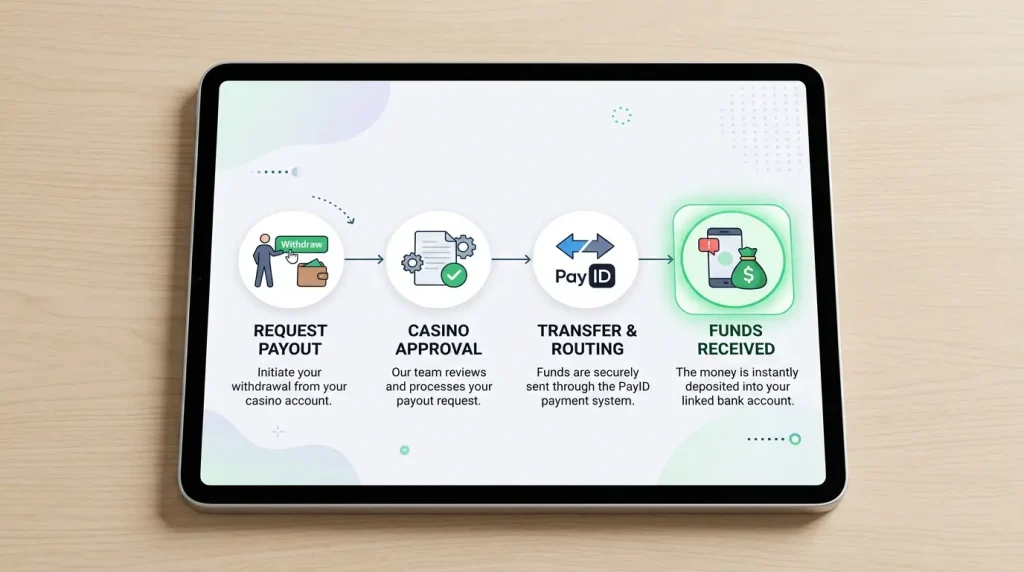

The real PayID payout timeline, step by step

Let me run you through a withdrawal the way it actually unfolds, because the advertised version skips the only part that takes time. Imagine you have won, your balance is verified, and you click withdraw. From that moment, four things have to happen, and only the last of them is fast.

First, the request enters a queue. The casino’s system logs your cashout and, depending on the operator, either auto-approves it within set parameters or flags it for manual review. Second, the review itself happens, where the operator confirms your identity is verified, your bonus wagering is cleared, and the withdrawal does not trip any risk threshold. Third, the operator initiates the actual payment. Fourth, the payment settles across the rail, and this final step is where the New Payments Platform earns its reputation. In 2024 the platform processed around 1.6 billion transactions worth roughly 1.99 trillion Australian dollars, the overwhelming majority of which cleared in real time. Once the operator presses send, the money genuinely moves in seconds.

The richness of the data PayID carries also matters here, in a way most players never notice. NPP transfers support data-heavy payment messages, with up to 280 characters of description attached to a transaction, which means a legitimate casino payout arrives with a clear reference rather than a cryptic code. That sounds minor until a withdrawal goes missing and you need to trace it, at which point a descriptive payment reference is the difference between a five-minute resolution and a week of back-and-forth.

So where does the time actually go? Almost entirely into steps one and two, the queue and the review. I have watched identical withdrawal amounts clear in under an hour at one operator and take three days at another, with the same rail underneath both. The variable is never the network. It is how the operator runs its approval process, how often it batches reviews, and whether it processes on weekends, which is the part the marketing never mentions.

The approval window vs the “instant” claim

If there is one concept that dissolves most withdrawal anxiety, it is the approval window, so let me give it the attention the casinos do not. The approval window is the gap between when you request a withdrawal and when the operator actually releases it to the rail. The rail then does its job almost instantly. The window is the wait.

The reason the rail is not the bottleneck is worth stating with numbers, because it changes how you should think about delays. The New Payments Platform handles more than 35 percent of all account-to-account transactions in Australia, the kind of volume that only works because settlement is genuinely real-time and reliable at scale. When your payout is slow, the rail carrying that 35 percent is not the thing struggling. The operator’s manual review, sitting in front of the rail, is.

This reframes the “instant withdrawal” claim entirely. An operator advertising instant payouts is, at best, telling you that once it approves your withdrawal, settlement is instant. That is true and also nearly meaningless, because you do not control the approval and it is the approval that takes time. The honest question to ask any operator is not “is it instant” but “what is your approval window, and do you process on weekends?” An operator that answers precisely is one worth trusting. An operator that just repeats “instant” is telling you it would rather you not look at the window at all.

Withdrawal limits and threshold reviews

I learned about threshold reviews the expensive way, watching a perfectly legitimate withdrawal freeze because it crossed a number the player had never been shown. Limits and thresholds are the second great source of delay after the approval window, and they operate quietly, which is exactly why they catch people off guard.

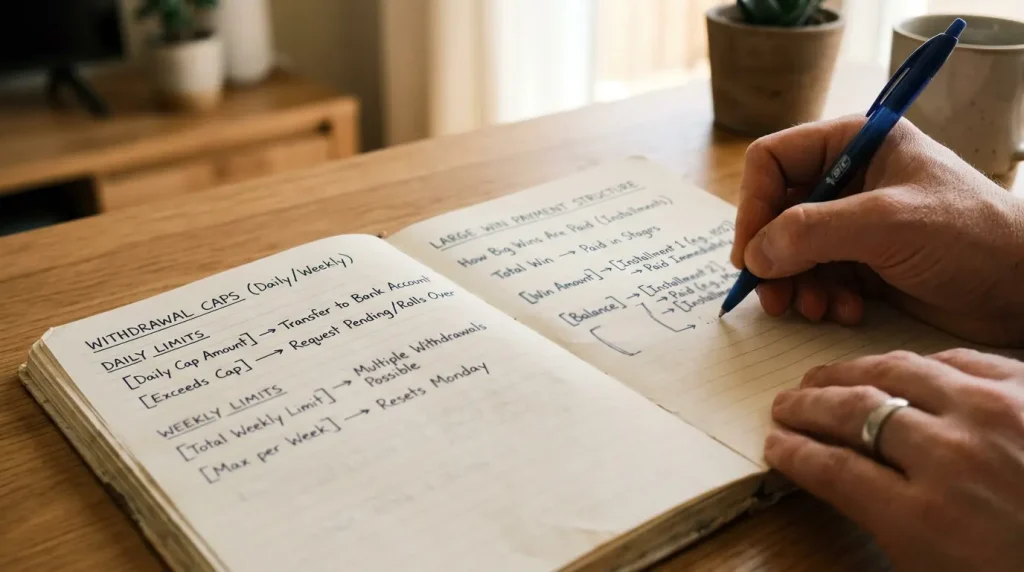

Most operators impose limits on how much you can withdraw per day, per week, and sometimes per month, and these limits are frequently lower than the deposit limits, which is itself a tell. If you win a sum larger than the daily withdrawal cap, the operator does not pay it in one go. It pays it in instalments across multiple days, each instalment subject to its own approval window. A large win that you expected to land in one fast PayID transfer can instead dribble out over a week, not because the rail is slow but because the operator’s limit structure forces it to.

Threshold reviews are the other mechanism, and they are tied to both risk management and compliance. When a withdrawal crosses a certain value, the operator triggers an enhanced check, which can mean additional identity verification, a source-of-funds query, or simply a slower manual sign-off by a senior reviewer. These reviews are not inherently sinister; legitimate operators run them to satisfy their own anti-money-laundering obligations. But an opaque operator can also use a threshold review as a delaying tactic, dragging out a large payout in the hope the player either gives up or gambles the balance back. The way you tell the difference is whether the operator can name the threshold and the expected review time in advance. A clear answer means a real process. A shifting, vague one means you should be cautious about how big a balance you let accumulate there.

The practical takeaway is to know the limits before you need them. Read the cashier terms for the per-day and per-week withdrawal caps and the value at which enhanced review kicks in, and size your expectations to those numbers rather than to the “instant” banner. A withdrawal that arrives in instalments over five days was never going to be instant, regardless of the rail, and knowing that in advance turns a frightening delay into a predictable schedule.

What slows a PayID payout down

Pull together everything that can stretch a withdrawal and you get a short, predictable list, which is genuinely good news, because predictable problems are manageable ones. Let me consolidate the causes so you can diagnose your own delay rather than panic about it.

The first cause is the approval window itself, the manual review the operator runs before releasing funds, which is the default delay on every withdrawal and the one you should always budget for. The second is incomplete identity verification, where the operator cannot release funds until your KYC, the know-your-customer checks that confirm who you are, is finished; this is why the first withdrawal at any casino is almost always the slowest, because verification happens once and then rarely again. The third is unmet bonus wagering, where a balance built partly from a bonus cannot be withdrawn until the playthrough condition is cleared, and the operator is correct to hold it. The fourth is withdrawal limits forcing a large win into instalments. The fifth is the operator simply not supporting PayID on withdrawal, routing you onto a slower bank transfer instead.

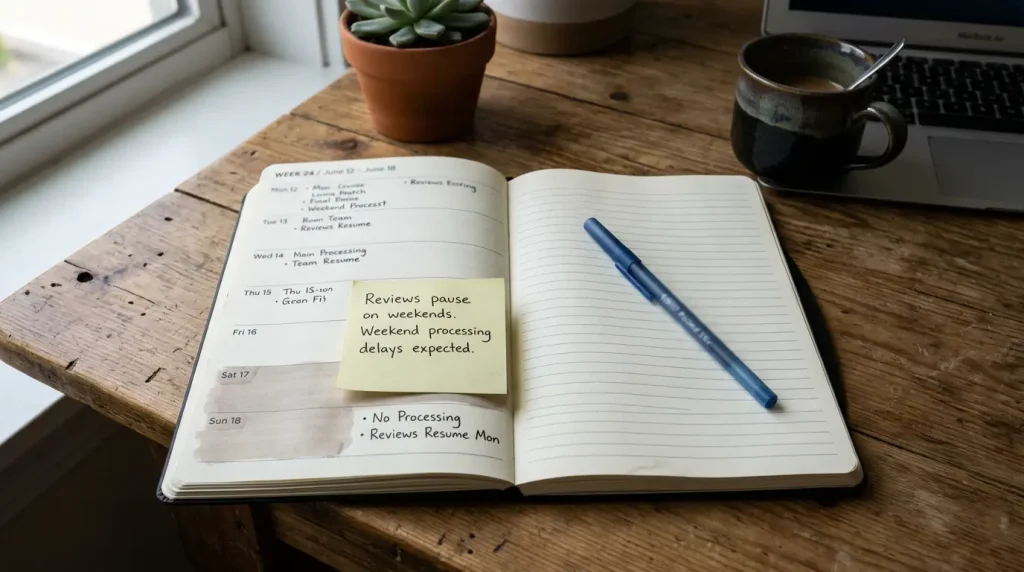

Weekend processing deserves its own mention because it surprises people who assume real-time means around the clock. The rail does run continuously, but the operator’s review team often does not. A withdrawal requested on Friday evening at an operator that reviews payouts only on business days will sit until Monday no matter how fast the underlying network is. This is purely a function of the casino’s staffing, not the technology, and it is one of the most common reasons a payout that “should” have been instant arrives three days later.

Underneath all of these sits the legitimate reason the checks exist at all, which is worth naming so you do not read every delay as bad faith. The payments industry has deliberately built control and verification into how money moves, with one senior payments figure describing the aim as giving customers “greater control and confidence when making payments.” The same instinct that protects you from sending money to a scammer also means an operator pauses to verify before releasing a large sum. The checks are not the enemy. An operator that hides behind them to avoid paying is.

So how do you tell an honest delay from a stalling tactic? The honest delay is explainable and bounded. The operator can tell you which check is running, why, and roughly how long it takes, and the clock actually moves toward a resolution. The stalling tactic is the opposite: vague reasons that shift each time you ask, documents requested one at a time so the clock keeps resetting, and a withdrawal that never quite clears no matter what you supply. When I am diagnosing a reader’s stuck payout, that is the distinction I look for first, because an operator running a legitimate review will tell you what it is reviewing, while an operator buying time will keep the reason fuzzy on purpose.

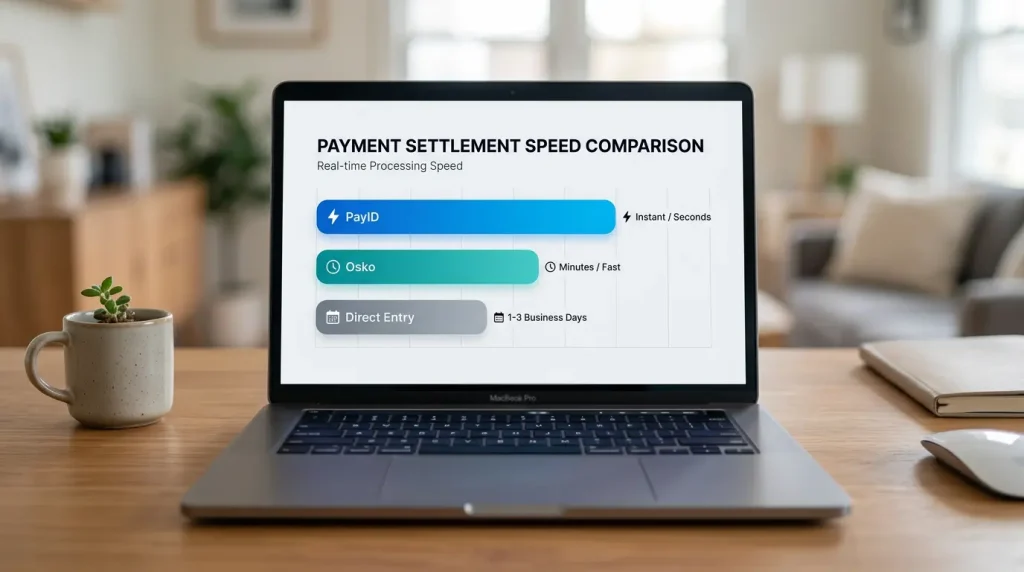

How PayID payout speed compares to other rails

Once you understand that the approval window dominates the timeline, the comparison between PayID and other withdrawal methods becomes clearer than the marketing makes it. The honest framing is that PayID is the fastest rail available for the settlement step, but the settlement step is rarely the part that was slowing you down.

Consider the economics that made PayID and its underlying platform ubiquitous in the first place. The wholesale cost of a single transaction on the network fell from 39 cents in 2019 to roughly 4 cents by the 2025 financial year, which is why real-time account-to-account transfers became the default plumbing for so much of Australian finance rather than a premium option. When a payout finally clears, PayID does it cheaply and instantly, with no card-network intermediary and no multi-day settlement lag.

That speed advantage is real but conditional, and the condition is the operator. A bank transfer payout and a PayID payout from the same casino, both gated behind the same manual approval window, will differ mainly in the final settlement step, where PayID wins on speed and the bank transfer adds a day or more. But a PayID payout with a slow operator can easily lose to a bank transfer payout from a fast one, because the approval window swamps the rail difference. The rail sets the floor on how fast you could be paid; the operator sets the ceiling on how fast you actually are.

It helps to remember how normal this rail has become, because it reframes PayID from an exotic casino feature to everyday infrastructure. By 2023 roughly one in three Australians had already used PayID for personal transfers, which means the technology paying out your winnings is the same technology people use to split a dinner bill. There is nothing experimental about it. When a PayID withdrawal is slow, it is not the unfamiliar new method failing; it is a mature, reliable rail being held back by an operator that chose to make you wait.

Getting paid faster, realistically

The single most useful shift you can make is to stop measuring withdrawals against the word “instant” and start measuring them against the approval window, because that is the number you can actually influence. Complete your identity verification early, before you ever request a withdrawal, so your first payout is not the slowest. Clear any bonus wagering deliberately rather than accidentally. Keep your expected payout under the daily withdrawal limit where you can, or accept in advance that a large win arrives in instalments. And request withdrawals early in the business week at operators that do not process on weekends.

Most of all, choose an operator that pays out through PayID in the first place and states its approval window plainly, because no amount of player discipline overcomes an operator that routes you onto a slow bank transfer by design. The rail underneath PayID is genuinely one of the fastest payment systems in the world, settling in seconds at a cost of a few cents. If your money is taking days, the network is not the reason, and now you know exactly where to look instead.

Frequently Asked Questions

Why was my PayID withdrawal sent as a regular bank transfer?

Because the operator accepts PayID on deposits but does not pay out through it. This is extremely common with offshore casinos, where inbound PayID is fast, irreversible and cheap to process, while outbound PayID requires the operator to maintain a funded account on the same rail. Rather than do that work, many operators route every withdrawal onto a generic bank transfer they were already set up to send. The deposit experience never guarantees the withdrawal experience, which is why you should confirm two-way PayID support before funding an account.

Can I speed up a pending PayID payout?

You can remove the delays that are within your control, though you cannot shorten the operator's approval window itself. Complete your identity verification before you request the withdrawal, since the first payout is usually slowest because checks happen once. Clear any bonus wagering fully, keep the amount under the daily withdrawal limit to avoid instalments, and request early in the business week at operators that do not process on weekends. Beyond that, the manual review sits with the operator, and no amount of contacting support changes how fast it chooses to run that review.

Is there a minimum amount I can withdraw via PayID?

Most operators set a minimum withdrawal amount, and it varies by casino, so check the cashier terms rather than assuming. The minimum is usually modest, but it exists, and a withdrawal request below it will simply be rejected or held until your balance clears the threshold. Pay equal attention to the maximum daily and weekly limits, because those are what force a large win to pay out in instalments over several days regardless of how fast the underlying rail settles.

Does weekend processing affect PayID payout time?

Yes, and it surprises people who assume real-time means around the clock. The New Payments Platform underneath PayID does run continuously, but the operator's review team often works business days only. A withdrawal requested on a Friday evening at such an operator will sit untouched until Monday, no matter how fast the network is, because the delay lives in the manual approval window rather than in settlement. If fast payout matters to you, request early in the week and favour operators that explicitly process withdrawals on weekends.

Recommend

Is PayID Safe for Online Casino Play? The Honest Answer

How safe PayID is, and what safety means here I have lost count of how many times someone has asked me "is PayID safe" and been quietly frustrated by my…

Are PayID Casinos Legal in Australia? Reading the Law Straight

The legal status of PayID casinos, stated plainly I am not a…

PayID Casino Australia: How the Payments, Safety and Legality Really Work

How a PayID Deposit Works at an Online Casino

Making your first PayID deposit The first time I ever funded a…

Playing Real-Money Pokies With PayID

Playing pokies with PayID Pokies are the reason most Australians end up…